Hop Notes 05: Reviewing the 2023 Acreage Strung Report

Updated 6/21. Expert analysis to help you make better hop decisions.

Each spring the United States Department of Agriculture’s (USDA) National Agricultural Statistics Service (NASS) releases the Hop Acreage Strung for Harvest Report. This report serves as a pre-harvest peek at how many acres will be harvested, of what varieties, in ID, OR, and WA.

The 2023 Acreage Strung Report has been hotly anticipated - why?All the conversations about the need to reduce hop production to prevent the 40M pound excess hop bubble bursting come down to this report. How many acres did the industry cut? In what varieties? In what states? How many acres shifted to other varieties? And what does this mean for the future of the hop market? Lets dig in.

The Numbers

Here is a link to the report. The hop section is on pages 7 and 8.

Total aggregated acre changes by variety:

Idaho specific acreage changes:

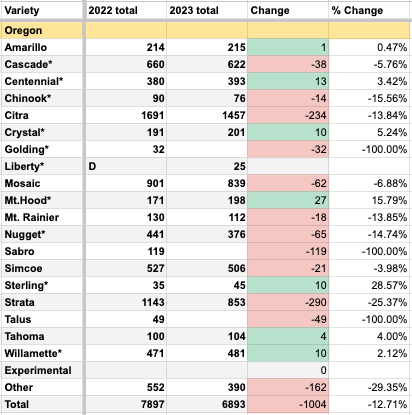

Oregon specific acreage changes:

Washington specific acreage changes:

Questions —> Answers

Q: How many less acres were strung this year?

A: 5,567 less total acres. Which is roughly half of the 10,000 acre goal set out at the USA Hops Conference merchant panel last year.

Commentary:

However, going one step deeper using farmer-level knowledge as Claire Desmarais of CLS Farms did in the latest Hop Talk blog post, that 5,500 acre net loss is probably more like 8-9,000 less aroma acres with a coinciding increase of 3-4,000 alpha acres. The target of the 10,000 acre trimming was aroma acres. The goal was to get annual aroma hop supply below annual aroma hop demand in order to start to push some of the 40M extra pounds of hops through the market. 8-9,000 less aroma acres should be close to being below annual demand. This means brewers may see shortages of needed varieties as soon as the 2023 harvest. Expect to be using more 2022, 21, or 20 crop years to make up that difference.

Still, the market remains on track for trouble with 40M pounds looming in the background. What if this is a great growing year and yields are up? Or craft beer (and hop demand) softens? Those extra hops will wind up on the pile. The taller that pile gets the greater the potential for a crash or burst in prices, which would lead to dramatic supply cuts, an eventual working through of the excess, and then a lag as supply looks to grow back up. That’s a harmful cycle that could take years to progress and hurt farmers, brewers, drinkers and even marketers before it completes.

Given declining craft beer trends and the loss not quite getting to 10,000 aroma acres the 2023 acreage change is probably not enough to make a big dent in the expensive and accumulating 40M pound excess inventory. This makes me believe that US hop acreage will continue to fall in the future.

I want to note here some important distinctions in language - acreage ‘cuts’ vs what I’ll call acreage ‘reductions’. Cuts are forced idling or removal of proprietary acres at the request of the variety’s owner. Reductions are voluntary idling or removal of hop acres with the decision made by the farmer. Maybe this is pedantic, and certainly the motivations for changes are not outlined by the USDA report, but it is important to consider when looking at these numbers. These numbers are more than just data points. They are a story about power, priorities, and market expectations.

Q: What varieties lost acres? Which ones gained?

A: As expected the biggest loser was Citra® down 3,200 acres (27%). Mosaic® was the second biggest loser down 1,344 acres (20%). The biggest winners were two high alpha varieties: CTZ (up 1,960 acres, 43%) and Pahto® (up 555 acres, 32%).

Commentary:

As covered in Hop Notes 02 proprietary varieties were the most over planted and are the most closely controlled, it is not a surprise to see these get the biggest cuts.

Other notable acreage declines include:

Cascade dropping nearly 800 acres (-15%) overall, there was some talk that Cascade would be up this year. Chinook also fell 15%.

Three notable public aroma varieties also saw major declines: Cashmere (-47%), Comet (-34%), and Triumph (-55 acres, the entirety of it’s reported acres). FYI this does not mean Triumph is gone from the face of the planet. It just means that the line item reported Triumph fields were removed. Triumph still has acreage but it is now in the opaque ‘Other’ bucket.

Sabro® continued its spiral, down 443 acres (66%).

El Dorado® also continued to drop, down 372 acres (31%).

The increase in CTZ and Pahto® and a few others means an additional 3-4,000 alpha acres entering the alpha market, which heading into this season, was seen as healthy (only needing ~+500 acres to find balance). The impact of additional supply entering this corner of the market will be interesting to watch.

Other notable acreage increases include:

Centennial bumping up 113 acres or 4%.

Sterling was up 10 acres (28%) which is good news for all 12 Sterling stans in America.

Crystal was up 73 acres (38%) which is good news for myself and the other 11 Crystal stans in America.

Willamette was up 102 acres (10%) and Mt.Hood was up 140 acres (66%) which along with the slight Sterling increase gives some foreshadowing to the always-coming never-here ‘year of the craft lager’.

Q: How did public hop acreage change comparer to private acres?

A: 6,992 private acres were cut and 1,072 were added, a delta of -5,920. While 2,428 acres of public hops were added and 1,831 were removed, a delta of +597.

Commentary:

That net increase of 597 public acres is the first time since 2020 that public acres have increased. It will be interesting to see if this trend continues as US hop acreage likely shrinks again next year.

Because merchants closely control the supply of private acres, and public acres tend to shift based on market expectations, the delta between changes in private acres and changes in public acres is a short hand way to view merchant versus farmer decision making. This year’s data shows me merchants were more aggressive in making cuts and there was some pushback from farmers in opting to plant more public hops (even if it was nearly all towards alpha-first CTZ variety).

Q: How did different states fair in the cuts?

A: Overall Oregon had the biggest percentage loss, Washington the largest amount of acres removed, but Idaho saw the steepest cuts in valuable proprietary allotments.

Commentary:

Pre-report conversations led me to expect to see Idaho farmers get the largest cuts in Hop Breeding Company (HBC) acreage. Farmers in Idaho saw their Citra® cut by 45% and Mosaic® cut by 25%.

WA farmers saw a 26% cut to Citra® allotments and 22% cut to Mosaic®.

Farmers in OR had 13% of their Citra® and 6% of Mosaic® cut.

Why Idaho? Idaho farmers tend to be newer to the generational game of hop growing than the other two major states and wind up with the short end of the stick when push comes to shove. There is no farm-level reporting on how cuts were doled out in each state to each farmer, but it is my fear that farmers who are more independent from the big proprietary owners got the worst of it.

The cuts that farmers in any state received to allotments of Citra® and Mosaic®, two of the most valuable American hops, are big blows to their operations. Imagine your distributor dropping 25-45% of your core brand volumes overnight.

Here’s a few things you can do if you are a brewer who wants to help support farmers in this difficult time:

Incorporate a broader diversity of American hop varieties into regular use.

Seek out a wider pool of ownership models and companies, specifically supporting public hops.

Source from multiple suppliers and/or direct from the farms.

The bottom line is your hop purchasing decisions have real impacts on the livelihoods of farmers.

More hop content:

Brewing With Vista is the latest MBAA podcast and features a panel of brewers talking about their experiences with Vista hops, including yours truly.

Ever wondered what it is like farming hops in Minnesota? Subscribe here for a monthly newsletter from the Minnesota Hop Growers Association with crop updates from hop farmers across Minnesota.

Farmers have a front-line role to play in adapting to and mitigating the impacts of climate change. CLS Farms covers some of their efforts to adapt in this post.

Thanks for reading Hop Notes 05. I hope you enjoyed it. If you did, please consider subscribing or forwarding it to a friend.

That’s all for now. If you have topics you’d like to read about in Hop Notes my inbox is open 24/7: ericsannerud@gmail.com.

Thanks for the insights, Eric. We appreciate your work!